Maria Municchi of M&G outlines the concepts behind building sustainability into a multi-asset strategy

Pension schemes looking to deliver retirement incomes...

Report

|

Dr Henrik Pontzen |

Dr Henrik Pontzen of Union Investment discusses a number of regulatory, market-driven and other factors that are coming into play for investors who are incorporating ESG concerns into their decision making

The rise of the once niche subject of sustainability has been impressive. Just a few years ago, it was hovering on the fringes of global asset management and was considered primarily as relevant to certain investor groups such as the church. Now, however, it is very much in the mainstream. And there are sound reasons for this rise, as sustainability criteria have a positive impact on investment success. ESG factors have become firmly anchored in the investment process. One key objective is better risk management. Another is to use ESG research as a tool that helps us to identify key industries of the future and to seize investment opportunities early on.

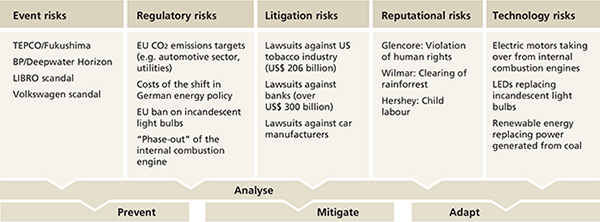

Many events in the recent past have clearly shown that there are a number of risk factors that can influence share prices but cannot be sufficiently explained by traditional patterns. These include litigation risk, regulatory risk, reputational risk and event risk, as illustrated by the catastrophe involving BP’s Deepwater Horizon oil rig, the network of corruption at Brazilian oil giant Petrobras and the VW emissions scandal. Each of these four risk categories presents a potential threat to the portfolio that is not adequately covered by the classic company analysis that has been standard practice for decades.

Anyone integrating sustainability criteria into their investment process is first and foremost adding an additional risk management filter. After all, problems such as carbon emissions, poor working conditions or insufficient controls in a company do not arise suddenly; there will have been warning signals beforehand. In-depth ESG analysis brings these problems to light at an early stage. Sustainability specialists and portfolio managers should therefore work in tandem as part of an integrated research process in order to boost the fundamental securities analysis with ESG factors and enable such risks to be reflected in investment decisions.

These decisions are not always focused exclusively on how to avoid potential risks. A key consideration is the question of whether and to what extent any identified risks have already been priced in by the market. Sometimes, the markdown on a security can be excessive and the assessment thus identifies a potential purchasing opportunity. This can happen, for example, if potential fines or revenue losses are overestimated by market participants.

Figure 1: Incorporating ESG risk assessment into the investment process

Source: Union Investment

Better insight into successful business models

Taking sustainability criteria into account helps asset managers to avoid losses, but also to tap into significant opportunities. And besides the risk situation, there is another major reason why ESG research is hugely beneficial to portfolio management – and thus to an asset manager’s customers. Examining sustainability criteria provides a better picture of whether a business model is feasible. In-depth knowledge of future emissions standards, for example, makes it possible to properly assess which companies in the transport sector will lead the way in this area. And anyone who knows about demographic change and the ensuing health problems for the population at large is better placed to gauge future demand for medical products. Whenever a sector or region faces disruptive changes, there are good opportunities for market players to stay ahead of the pack by using ESG research as a leading indicator. This applies to a whole host of core issues that, a few years ago, investors did not yet know were relevant: energy efficiency, water filters, LEDs as a replacement for old light bulbs, electric-powered transport and the accompanying optimisation of battery technology. These are just some of the areas that show how the clear trend towards managing resources efficiently has led to new future-oriented business models that are often highly profitable. Those who make the effort to gain a deeper understanding of these topics will be better equipped to gauge the potential of future technologies. This creates a valuable opportunity to get a head start on other investors in key industries – which should, ideally, be reflected in the performance of the securities.

Companies in dialogue

As important as research and analysis are to investment performance, a sophisticated sustainability strategy amounts to much more than this. Constructive and direct dialogue with companies is just as vital. Close contact and a strong working relationship with senior management provide the opportunity to address deficiencies regarding both ESG and other factors. In practice, this paves the way for dialogue on matters such as risks in the supply chain or at certain production sites. Potential shortfalls in governance structures must also be discussed, for example when vacancies on supervisory boards are due to be filled. Another engagement instrument is voting at annual general meetings. Here too, the goal is to raise companies’ awareness of the relevance of sustainability, strengthen their corporate governance structures and thus minimise the risks for both the company and its shareholders.

Increasing regulatory pressures

ESG matters are not expected to disappear from the limelight any time soon. This is because investors, particularly institutions, will come under increased pressure from regulators. Numerous initiatives are currently taking place at European level. Based on the findings of a group of experts at the EU,1 which presented its final report at the start of this year, work packages are currently being put together that are to become mandatory across Europe very soon. This plan of action will undoubtedly lead to significant changes for institutional investors. One example is the EU Shareholder Rights’ Directive, which has already been issued and must be transposed into national law by the middle of next year. It requires institutional investors to exercise their voting rights at annual general meetings. Pension funds, for example, will be forced to examine governance matters because they will have to justify their voting behaviour in the event of a crisis. Sustainability criteria will therefore inevitably become a greater factor in investment decisions. And that is definitely good news.

1. Technical Expert Group on Sustainable Finance

|

|

|